Fed Keeps Rates Unchanged, Denies Stagflation Concerns Despite Clear Evidence

Fed Keeps Rates Unchanged, Denies Stagflation Concerns Despite Clear Evidence

"Further progress on inflation is not assured and path is uncertain", repeated Jerome Powell during the press conference

Following the FOMC meeting on Wednesday, May 1st, Fed Chair Jerome Powell announced that the Federal Reserve decided to keep interest rates unchanged at 5.25-5.50% and cut Treasury balance sheet reduction to $25 billion.

Interest rate cuts will take longer than expected. No rate cuts in 2024 might be on the table.

Even though inflation has been increasing, Powell said it is "unlikely that the next policy move will be a rate hike” (of course the Fed won’t hike rates as the European Central Bank cuts rates):

Despite the fact that the economy has been cooling while inflation is still high (hint: stagflation), Powell said he “doesn’t really know” where concerns about stagflation are coming from, adding that he sees neither “stag” nor “flation” (hearing this from the Chair of the Federal Reserve should be concerning, to say the least):

"I was around for stagflation. It was brutal. Ten percent unemployment. High single-digit inflation. And very slow growth. Right now, we have 3% growth. Which is pretty solid growth, I would say, by any measure. And we have inflation running under 3%. So, I don't really understand where concerns about stagflation are coming from."

As GDP growth fell from 3.4% to 1.6% and inflation has increased for the second straight month, it’s clear Powell has defaulted to one of his favorite lines from the “inflation is transitory” playbook. The evidence of stagflation is overwhelming, yet Powell reminds us of the “2% target inflation rate” and that “the economy is strong”.

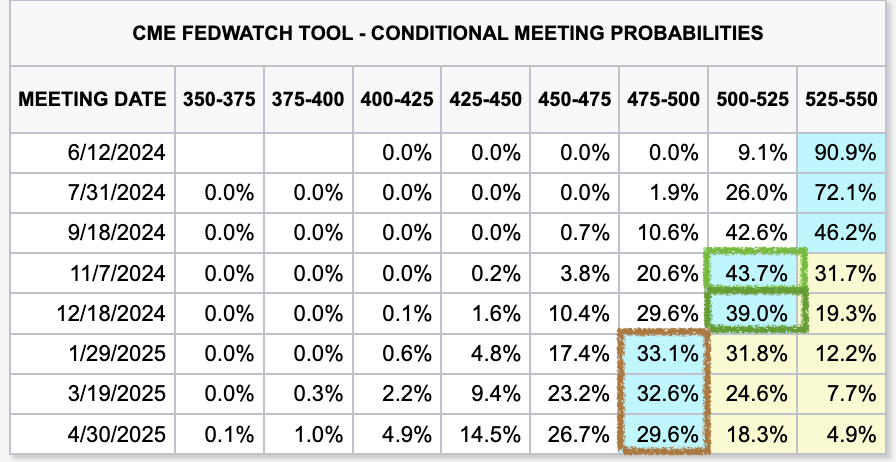

Following the announcement, interest rate futures are now expecting one rate cut in 2024 at the Fed's meeting on November 7, 2024, with a much lower possibility of another cut on December 18, 2024. Multiple interest rate cuts are expected in the first half of 2025:

Jerome Powell did hint at the upcoming labor market report likely not being “great”. He said “an unexpected weakening in labor market could warrant a rate cut”.

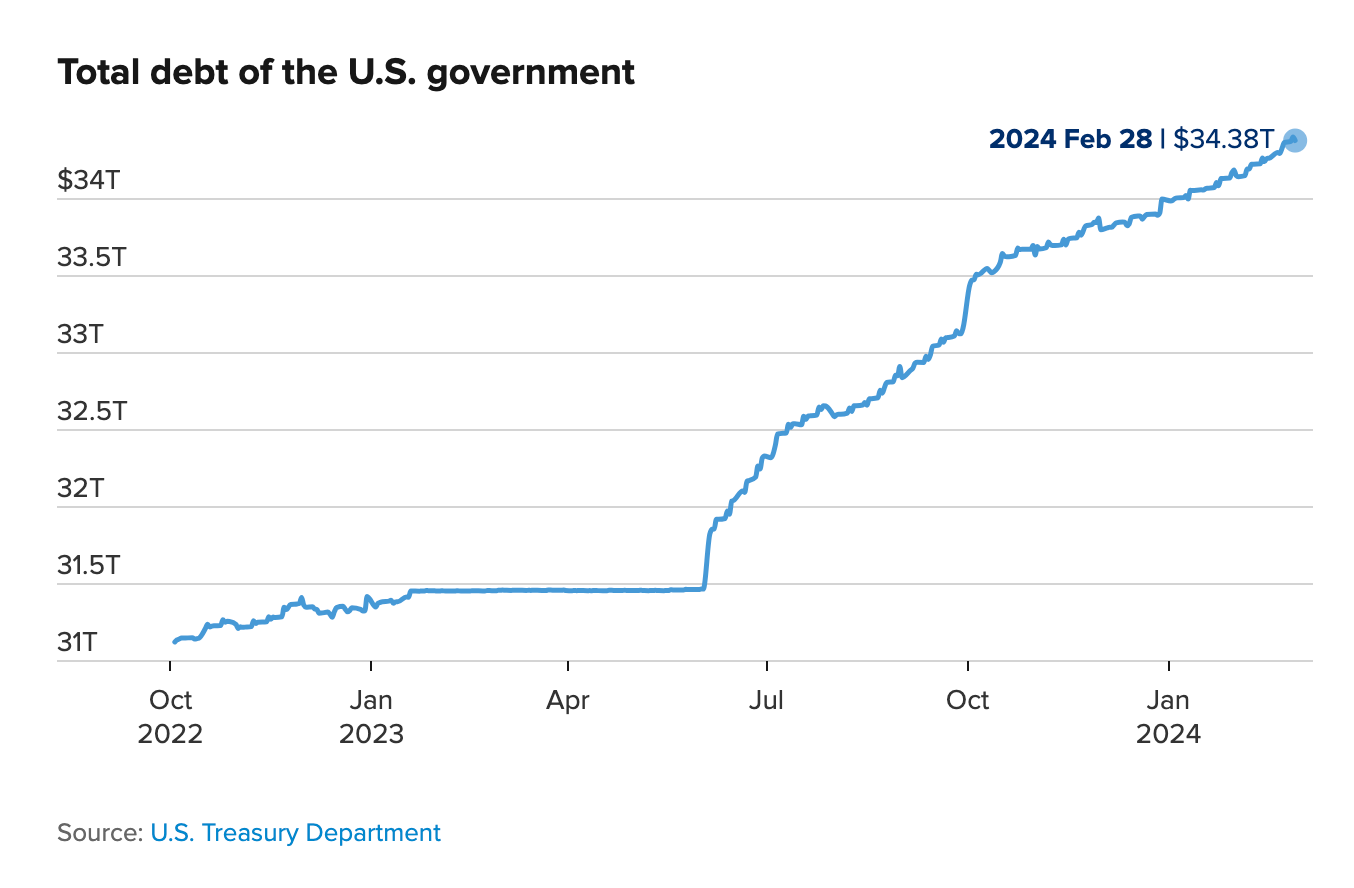

Keeping rates unchanged means that the government faces higher borrowing costs for longer. The US debt climbing roughly $1 trillion every 100 days and interest costs to service it are quickly becoming the top federal expense. As the government spending continues to increase and budget deficits hit record highs, the government will continue borrowing (at higher yields) to finance its spending.

So, to recap - inflation is not going anywhere any time soon, ie get used to higher prices; Biden’s budget proposal, if it goes into effect, will hike taxes in 2025 (including your UNREALIZED capital gains, as I discussed in a recent video) and unemployment numbers will likely rise as companies struggle with higher cost of financing and continue to cut costs to survive. It’s not a great outlook, but is anyone really surprised?

******

Like someone else said in the comments here, it seems as if it's being priced in that another Biden tenure is the play.

I could be dead wrong, but a part of me wants to think that once more banks start collapsing this summer, that might act as an alibi for Powell to say that's why they are lowering rates, but I guess we'll find out soon enough in June and July.

I have zero confidence in the Fed or its Chairman. Remember, it was Mr. Powell, along with another previous Fed Chair (now at Treasury), Yellen, who claimed inflation was transitory. If the supposedly wise economic minds at the Fed cannot get it right, why do we let them set interest rate policy? Does anyone believe the Fed has a magic ball to know what the incredibly complex American economy needs in terms of interest rates? They typically get it wrong more times than not, creating artificial bubbles in the process. The markets should be setting interest rates. Let the lenders and the borrowers determine if rates rise or fall by what they are willing to pay or receive. It certainly couldn't be worse than the Fed's guessing.